Unlocking Your Savings: A Guide to EPF Withdrawals

Imagine this: you're planning for a major life event – maybe it's buying your first home, funding your child's education, or securing a comfortable retirement. Suddenly, you remember the nest egg you've been diligently building in your Employees Provident Fund (EPF) account. The question arises: "How do I access these funds?" This comprehensive guide will walk you through the process of EPF withdrawals in Malaysia, equipping you with the knowledge to make informed decisions about your financial future.

The EPF, a cornerstone of Malaysia's social security system, acts as a financial safety net for employees. It operates on a simple principle: both employee and employer contribute a portion of the employee's salary towards their retirement savings. However, life doesn't always go according to plan. Recognizing this, the EPF offers several withdrawal options to cater to your various financial needs throughout different life stages.

Before delving into the specifics, it's crucial to understand the significance of EPF withdrawals. While these withdrawals provide a financial cushion during critical times, they also impact your retirement fund. Striking a balance between meeting your current needs and safeguarding your future financial security is paramount.

Navigating the world of EPF withdrawals might seem daunting, but it doesn't have to be. This guide aims to demystify the process, equipping you with the knowledge to make informed decisions about your hard-earned savings. We'll explore the various withdrawal categories, eligibility criteria, and step-by-step application procedures. Remember, understanding your options is the first step toward making sound financial choices.

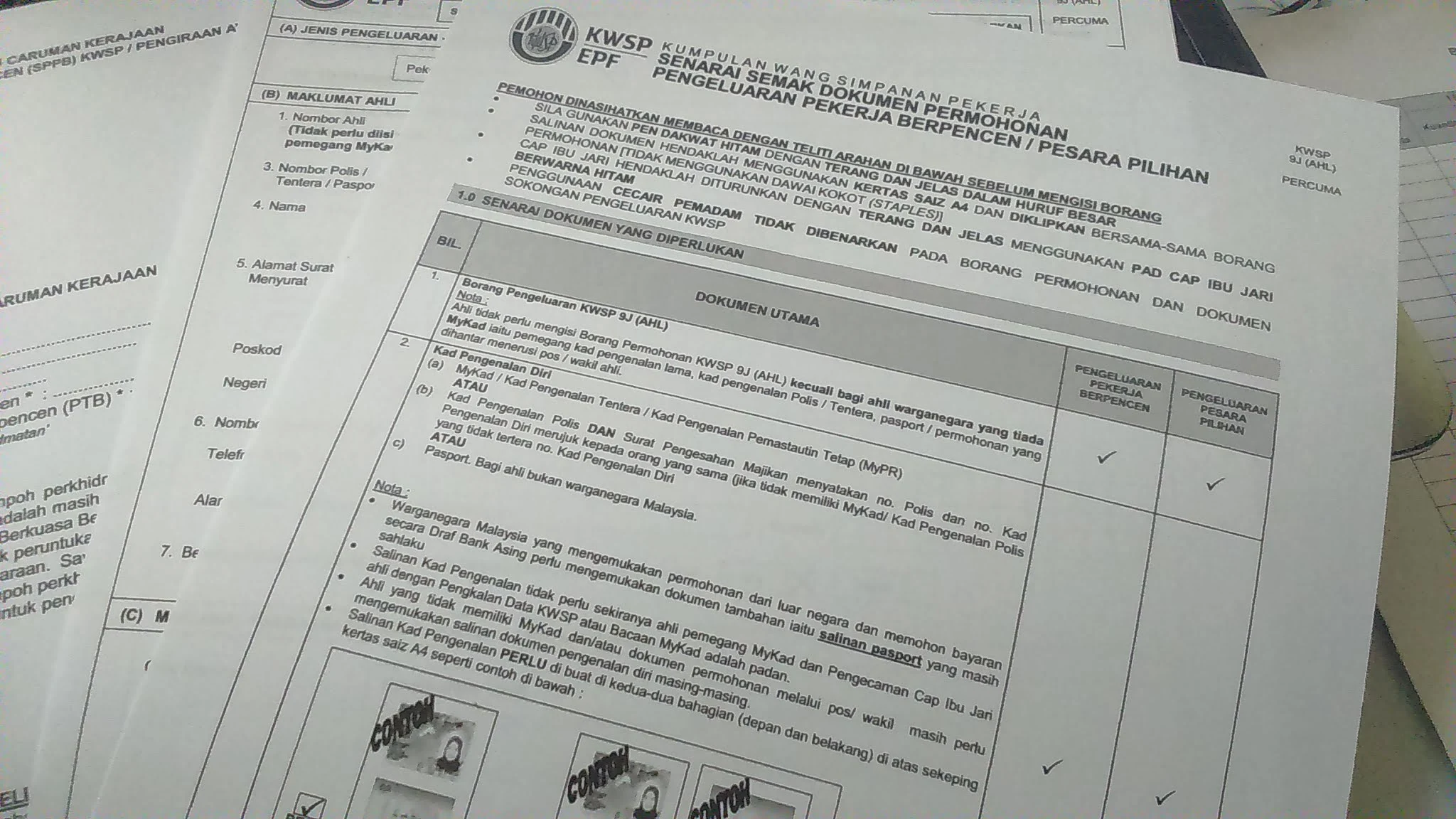

Understanding the various withdrawal categories is crucial. Whether you're withdrawing for housing, education, or medical reasons, each category comes with its own set of eligibility requirements and withdrawal limits. We'll delve into each category in detail later.

Advantages and Disadvantages of Withdrawing from Your EPF

Before making any decisions, it's essential to weigh the pros and cons:

| Advantages | Disadvantages |

|---|---|

| Access to funds for important life events | Reduces retirement savings |

| Financial relief during emergencies | Potential tax implications (depending on withdrawal category) |

| May help achieve specific financial goals (e.g., home ownership) | Missed opportunity for compound interest growth |

5 Best Practices for Withdrawing from Your EPF

To ensure you make the most of your EPF savings, consider these best practices:

- Withdraw only when necessary: Exhaust other financial resources before tapping into your EPF.

- Understand the withdrawal categories: Choose the category that aligns with your needs and eligibility.

- Calculate the impact on your retirement: Use the EPF calculator to estimate the long-term effects of your withdrawal.

- Explore alternative options: Consider loans or other financial assistance before opting for EPF withdrawals.

- Plan for replenishing your savings: If possible, devise a strategy to contribute extra funds to your EPF account after the withdrawal.

Frequently Asked Questions about EPF Withdrawals

Here are some common questions and their answers:

- Q: How do I check my EPF balance? A: You can check your balance online through the EPF i-Akaun portal, via the EPF mobile app, or at any EPF kiosk.

- Q: What is the minimum amount I can withdraw? A: Withdrawal limits vary depending on the category. Check the EPF website for specific details.

- Q: Can I withdraw my entire EPF balance? A: You can generally withdraw your entire balance upon reaching the age of 55, for specific health reasons, or if you are permanently leaving Malaysia.

- Q: How long does the withdrawal process take? A: Processing times vary depending on the withdrawal category and method of application. Online applications are typically processed faster.

- Q: What documents do I need for the application? A: Required documents vary by category but generally include identification documents, supporting documents for the specific withdrawal reason, and bank account information.

- Q: Can I withdraw from my EPF if I'm unemployed? A: Yes, certain withdrawal categories allow for withdrawals during unemployment, such as the withdrawal for reducing housing loan burdens.

- Q: Are there any tax implications for EPF withdrawals? A: Some withdrawals are tax-exempt, while others might be subject to taxation. It's best to consult the latest EPF guidelines or a tax professional for clarification.

- Q: What happens to my EPF savings if I pass away? A: Your nominated beneficiaries will receive your EPF savings. Make sure your nomination details are updated.

Tips and Tricks for a Smooth EPF Withdrawal

- Ensure your contact information with the EPF is up-to-date.

- Gather all required documents before starting your application.

- Apply online for faster processing times.

- Keep track of your application status through the EPF website or mobile app.

- Consult with the EPF customer service for any queries or assistance.

In conclusion, understanding how to navigate the process of EPF withdrawals is essential for any Malaysian seeking financial flexibility and security. By familiarizing yourself with the different withdrawal categories, eligibility criteria, and application procedures, you can make informed decisions that align with your current needs and long-term financial goals. Remember, your EPF savings represent an important investment in your future. While withdrawals can provide much-needed financial relief, it's crucial to approach them strategically, ensuring you strike a balance between meeting your present needs and securing a comfortable retirement.

Find the best october festivals near you

Lifting spirits a look at human connection

Casa de pensii cluj formulare your guide to romanian pensions